What if long-term income planning included options most people never hear about?

Free Educational Webinar

Preferred Retirement

A clear, education-first session that explores how some Canadians think differently about building wealth and income.

Beyond Savings Balances: Why focusing on "how much you save" is a blind spot, and how to shift toward sustainable cash-flow architecture.

Tax-Efficient Optimization: How to structure the capital you've already built to minimize annual tax erosion.

Bridging the Income Gap: Frameworks used to supplement CPP/OAS and traditional pensions for a 30-year retirement.

Strategic Asset Class: Why specialized structures are often treated as long-term financial foundations, not just "protection."

Save your seat

Register once and get access to the full educational webinar.

By clicking "RESERVE MY SPOT" below, you agree to receive educational reminders related to this webinar by SMS. Message and data rates may apply. Reply STOP to opt out at any time.

What happens next:

1) You'll receive a confirmation email with the access link.

2) You may receive reminders by email/SMS (if provided).

Educational only. We respect your privacy.

Not product advice. Individual circumstances vary.

Identifying Your Blind Spots is Only Step One

Awareness of oversights like high-interest debt or over-reliance on government benefits is critical.

For wealth-builders, the real challenge is integration.

The Need for a Structural Fix

A long-term solution isn't a product; it's a cash-flow architecture. This webinar reveals how to move to an integrated, tax-advantaged income map.

The "Account Balance" Illusion

As noted in Mistake #7, many focus on how much they save rather than how that money will provide income. This oversight leads to massive tax erosion.

The Reality Check

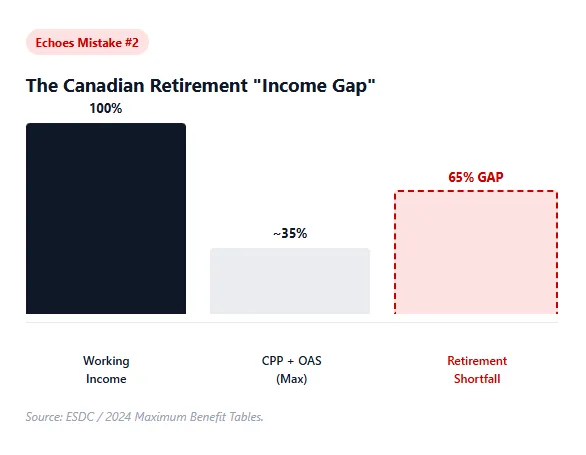

Retirement Looks Safer Than It Is

Relying on government benefits alone is a common oversight. Most assume "the system" will fill the gap, but typical benefits replace only a fraction of income for professionals.

To maintain your quality of life for 30+ years, your personal capital must be structured for maximum efficiency.

Readiness & Progress

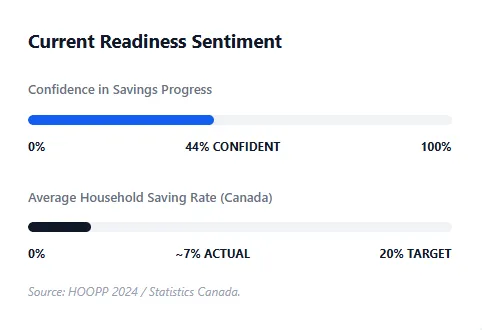

The Retirement Preparation Gap

Mistake #1 is waiting too long. For those who have started, the risk is "Inertia"—staying in low-growth strategies that can't outpace inflation (Mistake #6).

44% of Canadians are not saving for retirement at all.

The average household saving rate is significantly below required targets.

Readiness & Progress

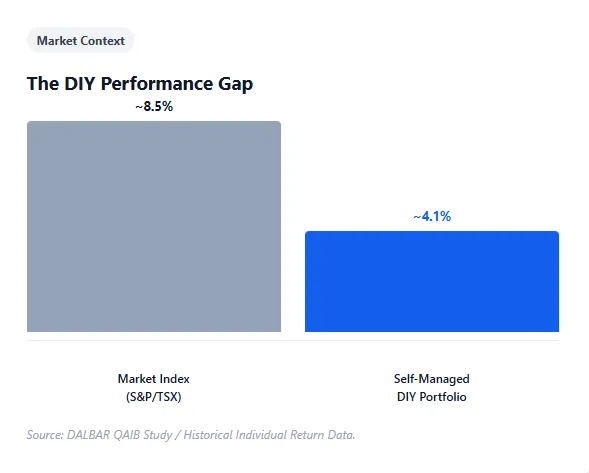

Why Individual Investors Trail the Market

While the "do-it-yourself" approach promises control, data consistently shows that individual investors capture only a fraction of market returns due to structural and behavioral friction.

The Behavior Gap: Buying during optimism and liquidating in fear destroys compounding.

Tax Inefficiency: Poor asset location leads to wealth erosion through avoidable taxation.

Implementation Drag: Lack of mechanical rebalancing causes portfolios to drift into higher risk.

The Silent Risk

Inflation & Purchasing Power

At a modest 2.5% inflation rate, the purchasing power of your money is cut nearly in half over a typical retirement.

$60,000 Today ≈ $108,000 in 25 Years

Required income just to maintain your current lifestyle.

The Silent Risk

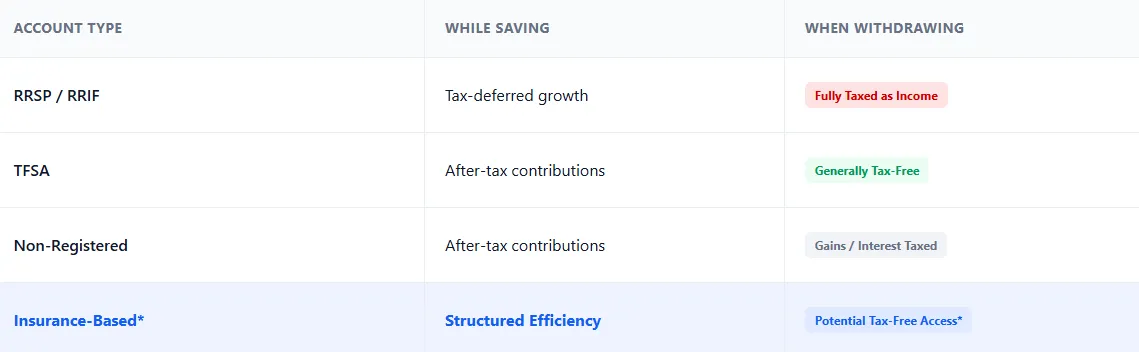

The After-Tax Reality

Retirement is a cash-flow problem, not a lump-sum problem. A long-term solution requires understanding how

different accounts interact during withdrawals.

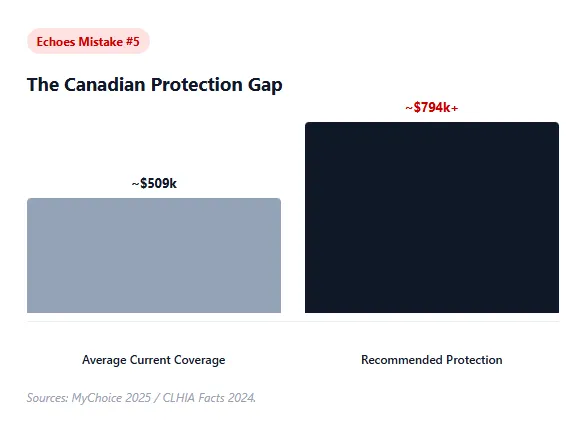

Insufficient Protection

A Silent Threat to Families

Treating protection as an option rather than a foundation is a critical mistake. Without it, a single life event can liquidate a lifetime of retirement savings.

42% of Canadians lack sufficient coverage for household debt.

Average households are under-insured by over $285,000.

Sustainable income planning starts with a robust protection plan.

The Long-Term Solution

From Identifying Blind Spots to Structural Clarity

Building a robust plan means moving beyond "saving more" and toward "structuring better."

Sustainable Cash Flow

Shift focus from raw account balances to long-term, predictable income streams.

Integrated Efficiency

Ensure growth, taxation, and protection work together instead of in disjointed silos.

Legacy Without Erosion

Preserve wealth for the next generation without losing a significant portion to estate taxes.

Reserve your spot

If you've ever felt that traditional retirement planning leaves out important options, this webinar will give you a broader, clearer perspective.

Educational discussion only. No obligation.

Financial education for Canadian families and professionals.

Resources

Legal

© 2026 ConnectHubPRO. All rights reserved.

This content is provided for general educational purposes only. It is not intended to provide legal, tax, investment, or individualized financial advice. Laws and practices may vary by province and are subject to change. Any examples are illustrative only and may not reflect your situation. Individual circumstances vary and suitability depends on the individual. Consider consulting qualified licensed professionals regarding your specific situation.